The cake is frosted. The flowers are fragrant. The champagne is chilled, and the décor is dreamy. You and your partner are madly in love and excited to start the next chapter in your lives. You’ve decided where to live, you’ve talked about your hopes and dreams and as you walk down the aisle, all you’re thinking about is what a perfect day to say: “I Do!.”

When you get married, you’re trusting that you know all you need to know about each other and are ready and willing to figure out any relationship bumps along the way. But have you had some frank financial conversations before tying the knot? Do you know if your partner has any debt and vice versa? Do you agree to joint bills? Joint investments? Full financial transparency? We’re guessing that finances are the last thing you’re thinking about on your wedding day but before you start your “happily ever after,” here are a couple of things to discuss to make the financial part of your marriage a bit easier.

Love is an Open Door

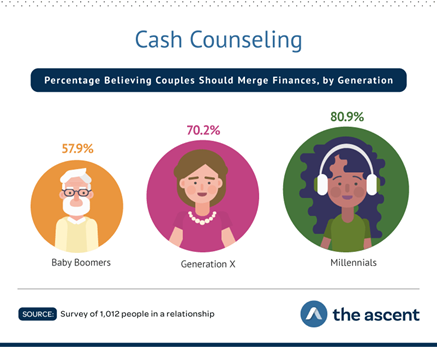

Talking about money remains taboo but when it comes to your spouse, honesty is the best policy. Do you know your partner’s financial situation and history? Does your partner know yours? According to a 2019 study, only about 30% of people were willing to share the amount of money they have in their bank account with a close friend.1 Compared to the Baby Boomer Generation, more Gen X and Millennials believe that couples should merge finances. Yet, despite a belief in more financial transparency, finances remain a source of strife for many relationships. As recently as 2018, 1 in 5 Americans said they have financial disagreements with their significant other at least monthly.2

We suggest that you start building financial transparency as a couple early. Discuss your student loans, other debt, your credit card history, and your credit score. Discuss your financial habits; is one of you a saver and the other a spender? If you were each to receive $1 million tomorrow, what would you do with it? Making sure you both understand the other person’s big picture will help inform your other financial decisions like how integrated you want your finances to be, who should be in charge of paying the monthly bills, etc.

Source: The Ascent Staff via The Motley Fool. https://www.fool.com/the-ascent/credit-cards/articles/study-the-financial-timeline-of-relationships/

Let’s Give Them Something to Talk About

We think that the name of the game for smooth financial sailing between couples is communication, communication, communication. However, we recognize that it’s easier said than done. 71% of couples say they communicate very well, yet nearly 40% of couples that live together are unable to correctly identify how much their partner earns.3,4 Money and, importantly, attitudes toward money remain a subject that makes people squirm and avoid at all costs. However, we think it’s necessary for couples to get down to the nitty gritty.

Try starting with a ten-minute weekly money conversation. This doesn’t have to be painful. Actually, we suggest making this fun (or at least rewarding yourselves with a fun date night afterward)! Here’s a short list of topics to get you started:

– What are each of your money habits?

– Do either of you have debt?

– What are your credit scores?

– Do you want to share bank accounts? Why or why not?

– Same for investment accounts.

– What are your risk tolerances? Are they aligned? Why or why not?

– What past experiences have shaped your money biases? Typically, our most formative years for our biases are between ages 16 and 25.

– Work together to write down a budget (and stick with it)!

Eventually we bet you’ll move on to weightier subjects like retirement goals and how to fund it, insurance needs and estate planning. We believe that actively keeping the lines of communication open and checking in with your partner about your long-term financial goals can help keep your financial boat sailing smoothly.

If I Had a Million Dollars

You’ve talked about your dream vacation and you know each other’s pet peeves. Maybe you’ve already decided who’s doing the laundry and who’s doing the dishes, but are you on the same page with your long-term financial goals? Do you want to leave an inheritance to a loved one or are you planning on spending every penny that you’ve earned? Is it more important to you to retire early or buy a second home?

Of the monthly disagreements over finances that many couples have, major purchases are the most common point of disagreement. Decisions to spend money now rather than saving for later put couples on a different page and can lead to a higher likelihood of divorce. One recent study suggests that feeling that one’s spouse spends money foolishly increased the likelihood of divorce by 45%! Talking over your financial goals and revisiting those goals regularly will keep you and your partner on the same page and your financial priorities aligned.5,6

Come Together

It’s almost inevitable that at some point in your relationship you and your significant other will have different incomes. Before you’re married, it can be helpful to self-reflect and talk about it. Each of you have money values and experiences that shape your beliefs and opinions about money. Discussing those values allow you each to better understand and support each other, especially when incomes are uneven. Remember, marriage is supposed to be a team sport!

While it might seem unsexy, creating a budget together can allow both people to feel equal in the financial decision making. It clarifies where the money goes and what discretionary income each person enjoys. Making your budget specific can also help align your financial goals. For instance, if the dream vacation is a safari in Africa, make saving for “African Safari” a specific item in your budget and you may both find yourselves excited to be saving together.

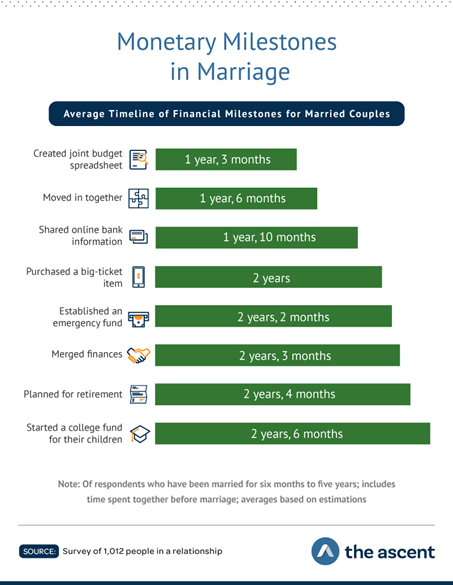

Lastly, although we think of budgets as money specific, it can also be helpful to create a “household chore budget.” Often neither person realizes how much the other contributes to making the household run smoothly. This can be even more true after you’re married and as life gets more complicated. The person who brings in less income may be contributing a much higher value in another area of the relationship. While a “set it and forget it” attitude might be tempting, many monetary milestones are reached and/or changed in the first few years of marriage. Remembering to revisit these conversations can help keep resentment from building up over time.

Source: The Ascent Staff via The Motley Fool. https://www.fool.com/the-ascent/credit-cards/articles/study-the-financial-timeline-of-relationships/

The last thing people want to think about when they are happy, in love, and planning a life together is divorce, but the ironic truth is that thinking ahead and being prepared for the worst can actually prevent it from happening. According to marriage.com, money is a leading cause for divorce, with 41% of marriages ending due to financial incompatibility. Even though it might be uncomfortable or awkward, having honest money talks before tying the knot is absolutely necessary to make sure you and your partner agree on important money matters.

If you are preparing to wed and need advice, or if you and your partner are looking for guidance as you begin a life together, please reach out to us. We’d love to be your second opinion.